Facebook’s full-frontal assault on finance

Simply sign up to the Digital currencies myFT Digest -- delivered directly to your inbox.

Flawed, derided, feared: Facebook’s proposal for a new virtual currency, revealed last week, has already provoked a backlash. But might it end up blowing the financial system wide open anyway?

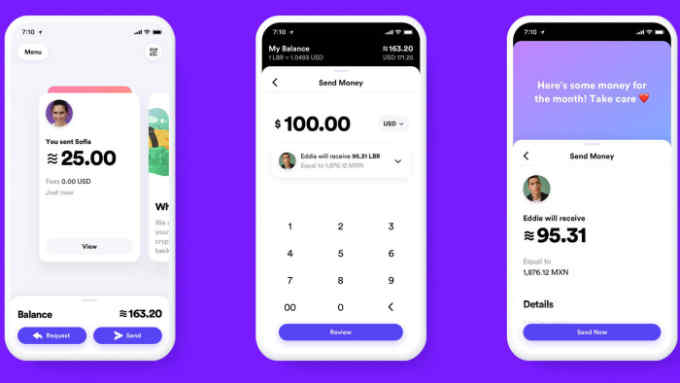

The idea marks a “long overdue” attack by Big Tech on the payments industry, says David Yermack, a finance professor at New York University’s Stern School of Business. Apple has carved out a limited role for its own payments system on the iPhone: by contrast, Facebook’s plan is a full-frontal assault. The planned launch, within a year, of its Libra digital currency would have the backing of partners like the payment networks Visa and Mastercard and internet companies Uber and eBay.

Facebook itself would create a “killer app” to take advantage of this digital money: a payment system embedded into its messaging services, so that users can easily and cheaply send money to friends or make purchases. With 2.4bn users, the social networking company could single-handedly propel cryptocurrencies into the mainstream, according to its supporters, fulfilling hopes first stirred by bitcoin a decade ago.

“The threat to the existing banks is severe,” says Mr Yermack. Companies like Facebook, Google and Amazon have two significant advantages over banks, he adds: they can process transactions at much lower cost, and they have proven themselves masters at creating new digital services, drawing billions of people to their platforms.

But the barriers to entry are also high and the resistance already extensive. Politicians, privacy activists and bankers have been among those lining up to question the proposal in the days since it was unveiled. That Facebook and its partners plan to forge ahead anyway is testament to how much is at stake.

The many criticisms and warnings stirred up over the last week have centred around three main areas.

The first concerns the credibility of Facebook itself. After the furore over Russian interference in the last US presidential election, including through content that appeared on Facebook, the social network is regarded with deep distrust. Mark Zuckerberg, chief executive officer, at first denied any responsibility, but has struck a note of humility as he tries to fix the social network.

But with its plans for a new cryptocurrency, Facebook’s unbounded ambition has been revived. The company has talked of reaching billions of people with its payment service. In an interview, Kevin Weil, vice-president of the proposed Facebook payment service, says the company hopes the new currency would last “hundreds of years”.

Even fans of the idea find it hard to believe Facebook can contemplate such a project, given the political and regulatory pressure it faces. Mamoon Hamid, a partner at venture capital firm Kleiner Perkins who has invested in a similar payments idea from messaging service Telegram, applauds the vision, but says: “Whether the world we live in wants them to do this is another matter. Things have changed over the past two years.”

Facebook executives have been at pains to stress that any financial services they create will be properly regulated. But it is already clear that the company hopes to skirt banking regulations, something that has antagonised executives in the sector.

Mr Weil says the company would look to offer other financial services such as credit but adds: “We’re not a bank, we don’t view ourselves that way. We’re not offering interest, for example, and things that banks do.” The distinction is one that many predict will not hold, as financial regulators subject the wayward internet company to heightened scrutiny.

There have also been questions about Facebook’s promise to keep its users’ financial information separate and not use it to target advertising. The sharing of data with other Facebook services would be possible if users opt in to certain services. And even without the opt-in, a Facebook service like WhatsApp would be able to see when a user makes a payment, as well as to whom, giving it valuable information.

Putting so much data in one organisation is asking for trouble, particularly given Facebook’s past failures, says Matt Stoller, a fellow at the Open Markets Institute, a Washington pressure group opposed to excessive concentration of corporate power. He also warns that Facebook would be in a position to leverage its dominant position in social networking to move into a new market — something that might be opposed by antitrust regulators.

The fact that more than two dozen other companies and organisations have already provisionally backed the Libra project, despite Facebook’s obvious political and regulatory challenges, highlights the scale of the opportunity.

For all its failings, Facebook, with its massive user base, could open the way to bringing cryptocurrencies into the mainstream. That has stirred hopes in Silicon Valley for a new generation of financial services, built on top of the new Libra backbone.

Many developers have been “sitting on the sidelines of crypto and really want to take the plunge,” says Katie Haun, a former US prosecutor who now runs a cryptocurrency fund for Silicon Valley venture capital firm Andreessen Horowitz. “This will be a catalyst for a lot of talent coming in to the space.”

The second major area of concern about Facebook’s plan stems from the nature of the currency itself, and whether it would leave too much financial power in the hands of a self-selected group of big companies. The plan calls for Libra to operate on a version of a blockchain — a decentralised ledger, maintained by all participants in the network, where transactions would be recorded.

Yet it would stop short of the ideal of decentralisation pioneered by the bitcoin blockchain, where anyone can validate transactions. That creates a permissionless system where no central authority decides who is worthy of trust. Public blockchains like this cannot operate at the scale and speed needed to handle the massive number of real-time transactions that will be required with Libra, says Avivah Litan, blockchain analyst at Gartner.

Instead, the Libra backers aim to create a private network of 100 companies that can be trusted to post transactions, without the need for any independent validation system. The promoters say they aim to start moving to a truly permissionless network within five years — although not everyone involved believes this will be technically possible.

Regardless of this limitation, Libra “is probably a much more efficient system” than today’s bank-controlled payment networks, Ms Litan says. “But it’s still controlled by the big corporations.” She and others warn that this would put considerable power into the hands of a group of private entities — particularly if Libra turns into the kind of global currency that Facebook hopes.

A closed private group like this could also invite an antitrust challenge, says Mr Stoller — particularly when it involves two duopolists, Visa and Mastercard, working together on a project.

For cryptocurrency purists, these shortcomings are serious. “It is not decentralised, so customers are at the mercy of Facebook, and it is not frictionless — it still uses the banking system and is tied to political currency,” says Tim Draper, one of Silicon Valley’s earliest backers of cryptocurrencies.

But even many people opposed to seeing Facebook launch a cryptocurrency accept that it could have wider benefits. Libra “has a great distribution channel in Facebook, and it provides a bridge for those who are not yet ready to convert all their transactions to bitcoin,” Mr Draper concedes. That could make it “a great interim step toward a fully open, truly global, transparent and frictionless currency like bitcoin.”

The third area of concern is whether a new currency like Libra could pose deeper systemic risks, while also interfering with the ability of central banks to police their financial systems and operate normal monetary policy. If so, governments and regulators may try to strangle it at birth.

Mark Carney, governor of the Bank of England, has made it clear that the potential systemic risks in a system like Libra will require it to be subjected to the highest levels of scrutiny.

By operating outside normal banking channels, critics warn it could be harder for governments to limit payments out of a country, or apply sanctions against a foreign power. “Any parallel currency to some extent undermines the sovereign institutions that control currency,” says Mr Stoller. “The reason this one seems particularly significant is because it’s Facebook. This isn’t just some libertarian dudes who hang out at strip joints, smoking weed and trading in bitcoin. It’s Visa and Mastercard.”

Some Libra critics say that it would also leave private corporations with undue influence over monetary conditions. Facebook and its allies deny this.

They point out that Libra will be fully backed by a basket of government-issued, or fiat, currency, meaning that the system would not create any new money. Instead, the fiat currency would sit in reserve, while its digital alter-ego is set free on the internet, bringing down transaction costs and supporting new types of services.

Yet mass adoption of the currency could still have distorting effects. Libra’s backers hope that a large number of people in the developing world opt to hold Libra deposits rather than their country’s currencies. That could weaken the power of the local authorities, who would have less influence over monetary conditions if many transactions in the economy were implicitly backed by foreign currency.

As Thomas Adrian, an IMF official, put it in a speech last month, countries with weak currencies might find it harder to muddle through in times of crisis: “One either makes it or is taken over by foreign e-money.”

Even without Libra, digital money systems backed by official currency have become widely used in some parts of the world. They are led by China’s booming mobile payment systems, run by Alibaba and Tencent — one reason why Silicon Valley, which is in a race with China’s tech leaders on the world stage, argue that regulators in Washington should not be too heavy-handed. “The genie is already out of the bottle with this technology,” says Ms Haun.

Some central bankers may be ready to engage with the new era of digital currencies. Mr Carney on Thursday said the Bank of England could potentially allow tech companies to store funds overnight at the central bank, giving them an alternative to leaving deposits with commercial banks.

Giving direct access to the central bank like this would bring down costs for these payments systems and put them on an equal footing with commercial banks. It would also bring central banks one step closer to issuing digital currencies.

The financial authorities have little choice but to try to adapt, says Mr Yermack. If they try to crack down on Libra or other projects like it, the tech companies could easily take their payment plans offshore.

As Libra’s potential shortcomings have been picked over, meanwhile, there has been less attention to how the digital currency — or other ideas like it — might affect the world of finance, were they to catch on.

So far, Facebook and other Libra members have sought to put the focus on cross-border remittances, where fees could be slashed, and the chance to offer basic financial services to the 1.7bn of people in the world who do not have a bank account. These represent the most politically palatable uses of the currency, and the ones most likely to win official support.

But the widespread use of e-money would also have broader implications. Just because financial services work “well enough” in many developed countries do not mean there isn’t plenty of room for improvement, says Ms Haun: “They’re slow, they’re inefficient, you pay middlemen along the way.”

Facebook appears to have something like this planned for Calibra, the payment service it hopes to launch on the Libra blockchain. Integrated into its messaging services, this would support a new era of online commerce.

A true digital currency has other advantages. It could be used for micropayments, according to Facebook, potentially bringing a new way for users to pay for digital content as they read it or watch it.

Further ahead, Libra’s backers say they plan to introduce “smart contracts” on to the network — arrangements where money changes hands automatically when certain real-world conditions are met.

How this might affect a future world where machine-to-machine communications and intelligent agents hold sway is the stuff of Silicon Valley fever dreams. It could lead to autonomous vehicles, for instance, that decide for themselves when it’s worth paying to move into an express lane, and handle the payment automatically.

Libra may never play a part in this imagined future. Worries about Facebook — along with inherent limitations in the project itself — could well doom it to failure. But as digital money systems spread to more corners of the digital world, the prospects for truly disruptive change in finance are rising.

Comments