Brazil counts success with Pix payments tool

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

At a stall selling fresh coconut water in a bustling São Paulo street market, customers have three payment options: cash, card or Pix.

The latter is an instant money transfer tool that has transformed day-to-day transactions in Brazil following its introduction almost three years ago.

“It’s much better — it’s faster, easier and fails far less,” says cashier Kleber de Jesus, as a colleague hacks a hole into one of the fruits.

He enters the amount on a card machine, producing a QR code on its screen. The customer opens a mobile banking app, scans the image and taps “confirm”. The money lands in seconds.

Amid a boom in financial technology launches across Latin America, that have brought basic banking services to millions for the first time, Pix has a strong claim to rank among the most impactful innovations.

To use it, an account with a bank, a fintech or a digital wallet provider is required. The service is mainly accessed using smartphones.

It is free for individuals and about two-thirds of the Brazilian population — some 140mn people — have used the app since it was launched by the country’s central bank in November 2020.

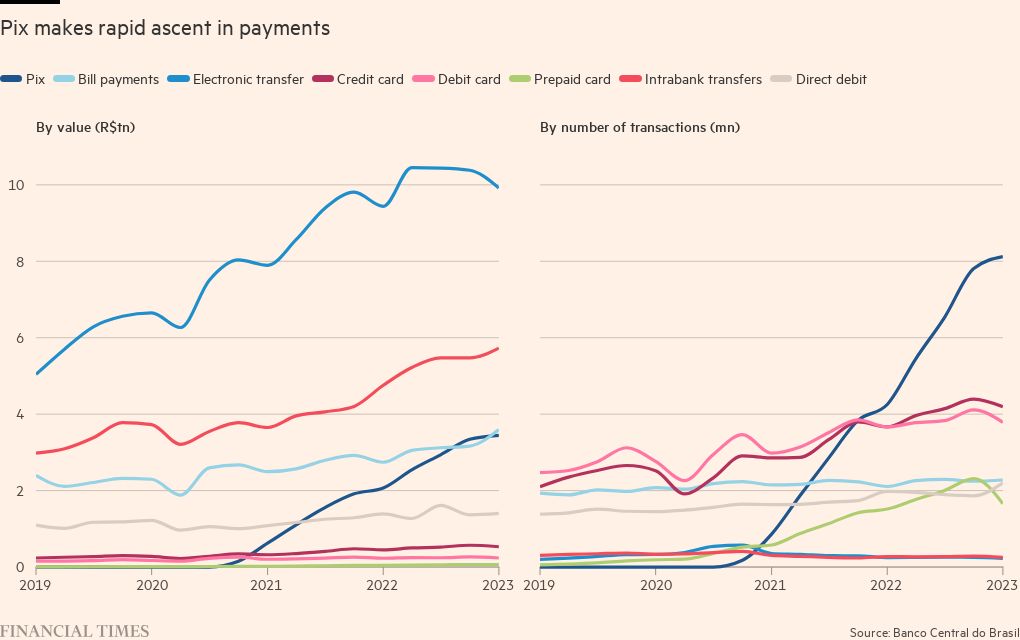

Pix is now the most common form of payment in the region’s largest economy by number of transactions, accounting for 29 per cent of transfers in 2022, according to central bank data on non-cash methods.

This month, it hit a single-day record of 153mn transactions that moved R$76bn ($15.3bn).

Mostly used for sending relatively small amounts, the digital tool is credited with boosting financial inclusion and cutting the cost of doing business for Brazil’s large informal workforce.

“Many people in the low-income bracket, small enterprises or micro-entrepreneurs rely a lot on Pix,” says Ceres Lisboa, senior analyst at credit rating agency Moody’s. “It brought more people into the financial system.”

Globally, Pix ranks as the second most-used real-time electronic transfer system, only after India’s United Payments Interface, according to a report by ACI Worldwide.

It was developed as a public sector solution to the shortcomings of the traditional fund transfer methods offered by Brazil’s banking sector. These often charge a fee, do not settle instantly, and only operate during working hours. Pix is available 24/7.

Angelo Duarte, head of the department of competition and financial market structure at the Banco Central do Brasil, says that, while Brazil lagged behind other countries in adopting a fast payment system, Pix “ended up becoming a leader in number of transactions. All of us here at the central bank were surprised by the speed of adoption”.

One aim of Pix was to reduce the use of cash and its associated costs across a vast territory such as Brazil’s, explains Duarte. In the process, it helped expand financial services to consumers who previously went underserved.

“Institutions — whether fintechs or traditional banks — started to know these people better in terms of income [and], after a while, began to offer them credit, insurance and investment products,” he says.

Proponents say the tool has also widened access to online shopping, since many Brazilian ecommerce sites do not accept debit cards.

It is not the only initiative to shake up payments in Brazil, however. WhatsApp launched a money transfer tool in the country in 2020, but it was temporarily suspended by regulators on concerns including competition and data privacy. Officials reject the notion that this was in order to favour the subsequent launch of Pix months later.

Still, to the taxpayer, Pix has proven relatively cheap: costing $4mn to develop and $8mn to run in 2022, according to the BCB.

All institutions with 500,000-plus customers must now offer Pix and, while it is free for consumers, charges can be made for businesses. Even so, for taxi drivers and street vendors, it typically works out cheaper than using wireless card machines, which can also be unreliable.

Users create a Pix identity number, or “key”, linked to their mobile number, email address or tax code, through which they are located in the system.

It is not uncommon to see these Pix keys written on placards begging for donations in the sprawling metropolis of São Paulo, Brazil’s financial capital, since homelessness began to rise after the Covid-19 pandemic.

The payments platform also allows the physical withdrawal of cash from participating commercial establishments or ATMs. An upcoming feature will enable a kind of direct debit for recurring bills and the central bank says that, in future, the tool could enable cross-border payments.

Pix has been a boon for digital entrepreneurs, according to Bruno Diniz, co-founder at financial innovation consultancy Spiralem. “It’s made it easier for many fintechs to flourish,” he says, citing online gambling and cryptocurrency exchanges as examples. “Some have surfed the popularity of Pix and even put it in their name.”

In a country where violent crime and scams are rife, it has also been seized on by organised gangs. This was highlighted by a spate of kidnappings in which victims were forced to transfer significant sums of money to perpetrators using Pix.

In response, the central bank imposed a transfer limit of R$1,000 in the evenings — which can be manually altered with a delay — and many banks have implemented their own safety measures. Duarte says the BCB is dedicating resources to tackling fraudulent accounts and improving security.

However, despite the rapid adoption of Pix, it still only represented 12 per cent of the value of non-cash money transfers last year.

Other forms of payments including debit and credit cards remain popular — the latter because of the option to pay in instalments. And analysts note that traditional bank transfers still dominate overall volumes and are often preferred by companies for larger sums.

Overall, then, Pix’s impact on established lenders has not been as detrimental as some had expected. Moody’s initially estimated it would dent bank fee incomes by 8 per cent, but senior analyst Lisboa says this did not come to pass. “As Pix gains more traction, the banks are creating services around it that will continue to compensate for the loss of these fees they had on transfers,” she says. “In the end, it’s more positive than negative for traditional banks.”

Comments