China’s debt isn’t the problem

Simply sign up to the Global Economy myFT Digest -- delivered directly to your inbox.

Michael Pettis is a senior fellow at the Carnegie Endowment and teaches finance at Peking University.

There’s naturally a lot of attention on China’s swelling debt burden, especially after Moody’s cut the outlook on the country’s credit rating based on the “broad downside risks” posed by the borrowing binge.

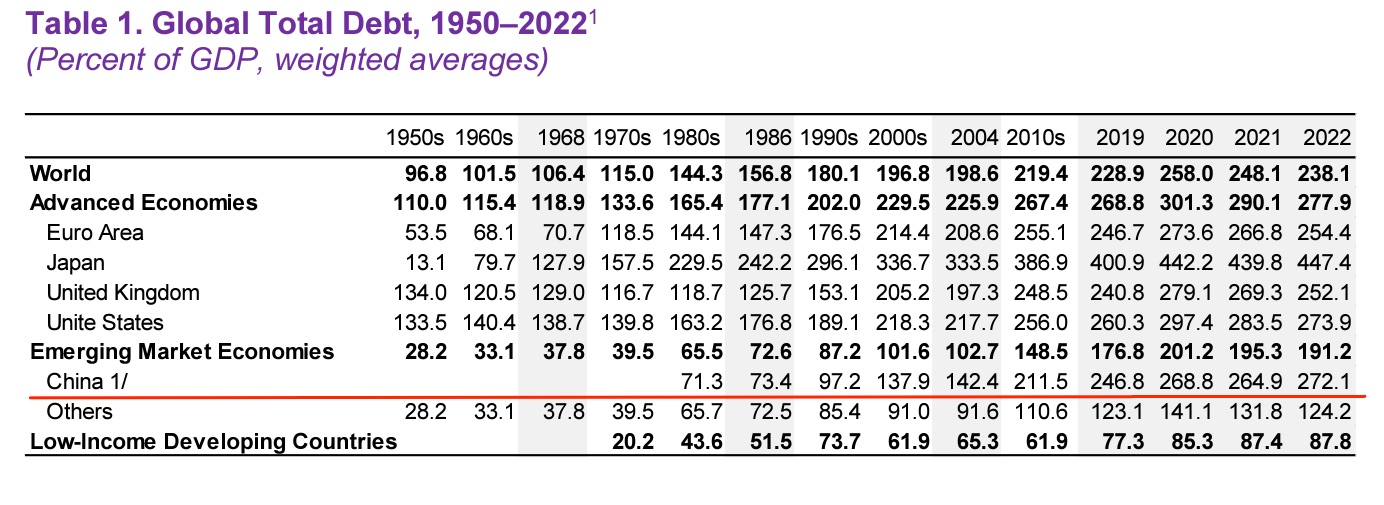

That’s understandable, given that the IMF in its latest Global Debt Monitor highlighted how China’s overall debt-to-GDP ratio has increased fourfold since the 1980s. It has been particularly rapid over the past decade. Over half of the increase in the entire global economy’s debt-to-GDP ratio since 2008 is solely due to an “unparalleled” rise in China, according to the IMF.

That $47.5tn total debt pile has grown further in 2023, which might mean that China has now finally overtaken the US in debt-to-GDP terms (zoomable version of the table below):

However, the surge in Chinese debt is not itself the problem but rather a symptom of the problem. The real problem is the cumulative but unrecognised losses associated with the misallocation of investment over the past decade into excess property, infrastructure and, increasingly, manufacturing.

This distinction is necessary because much of the discussion on resolving the debt has so far focused on preventing or minimising disruptions in the banking system and on the liability side of balance sheets.

These matter — the way in which liabilities are resolved will drive the distribution of losses to various sectors of the economy — but it’s important to understand that the problems don’t emerge from the liability side of China’s balance sheets. They emerge from the asset side.

That’s because the losses associated with the misallocation of investment over the past 10-15 years were capitalised, rather than recognised. In proper accounting, investment losses are treated as expenses, which result in a reduction of earnings and net capital. If, however, the entity responsible for the investment misallocation is able to avoid recognising the loss by carrying the investment on its balance sheets at cost, it has incorrectly capitalised the losses, ie converted what should have been an expense into a fictitious asset.

The result is that the entity will report higher earnings than it should, along with a higher total value of assets. But this fictitious asset by definition is unable to generate returns, and so it cannot be used to service the debt that funded it. In an economy in which most activity occurs under hard-budget constraints, this is a self-correcting problem. Entities that systematically misallocate investment are forced into bankruptcy, during which the value of assets is written down and the losses recognised and assigned.

But, as the Hungarian economist János Kornai explained many years ago, this process can go on for a very long time if it occurs in sectors of the economy that operate under soft-budget constraints, for example state-owned enterprises, local governments, and highly subsidised manufacturers.

In these cases, state-sponsored access to credit allows non-productive investment to be sustained. And as economic activity shifts to these sectors, the result can be many years of unrecognised investment losses during which both earnings and the recorded value of assets substantially exceed their real values. Because the debt that funds this fictitious investment cannot be serviced by the investment, the longer it goes on, the more debt there is.

But once these soft-budget entities are no longer able — or willing — to roll over and expand the debt, they will then be forced to recognise that the asset side of the balance sheet simply doesn’t generate enough value to service the liability side. Put another way, they will be forced to recognise that the real value of the assets on their balance sheets are less than their recorded value.

That is the real, huge and intractable problem China faces.

As long as local governments were able to increase debt at will, they could invest to meet excessively high GDP growth targets and could avoid recognising the associated investment losses. But once Beijing imposed debt constraints, either the fictitious assets would have to be written down and the costs allocated, or, which is the same thing, the debt would have to be serviced through transfers from other sectors of the economy.

Either way, someone would have to absorb the losses, and as this happens, there are at least three impacts on the economy.

The first impact does not involve the real welfare and value of the economy, but it may be politically embarrassing. It consists of reversing the former artificial boost to income. At the macroeconomic level, this means reversing the former additions to GDP.

The second impact consists of the unwinding of a previous “wealth effect”. Households and other entities that assumed they were wealthier than they actually were tended collectively to spend more than they could have otherwise afforded — in the case of local governments, this included spending on facilities, employees and services. Once they are forced to recognise their reduced wealth, however, they must cut back on spending, with adverse effects on the economy.

The third and most important impact is what finance specialists call “financial distress” costs. In order to protect themselves from being forced directly or indirectly to absorb part of the losses, a wide range of economic actors — workers, middle-class savers, the wealthy, businesses, exporters, banks, and even local governments — will change their behaviour in ways that undermine growth.

Financial distress costs rise with the uncertainty associated with the allocation of losses, and what makes them so severe is that they are often self-reinforcing. As we’ve seen with the correction in China’s property sector, financial distress costs are almost always much higher than anyone expected.

The point is that resolving China’s debt problem is not just about resolving the liability side of the balance sheet. What matters more to the overall economy is that asset-side losses are distributed quickly and in ways that minimise financial distress costs. That is why restructuring liabilities must be about more than protecting the financial system. It must be designed to minimise additional losses.

In China, as in other countries, it is usually not the debt itself that is the main problem. Debt is just a transfer, and does not necessarily entail the assignment of losses. What matters is the value of fictitious assets that back the debt.

That’s why Beijing should focus not just on managing the liability-side consequences of excessive debt in the system but also (and more importantly) on the asset-side consequences. It must recognise the full extent of the losses and move quickly to allocate them in the most economically and politically efficient ways.

Postponing this recognition and focusing mainly on minimising financial disruption, as Japan did in the 1990s, will just increase the overall cost to the economy.

Further reading:

— China’s Japanification (FTAV)

— The great Chinese flow reversal (FTAV)

{kind=link}

Comments