How rising interest rates are exposing bank weaknesses

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

The end of historically low interest rates was billed as good news for banks, which make more money as the difference widens between what they charge borrowers and what they pay for funding. But recent crises on both sides of the Atlantic show that the reality is more complex, upending the conventional wisdom.

Some banks, notably in Europe, are stuck with big loan books at interest rates fixed far below current levels. Others with a higher share of their book at variable rates can immediately charge more for outstanding loans but risk a wave of defaults from borrowers who can no longer afford to service their debt.

Then there is the issue of government bonds, where banks have been holding ever more of their liquidity after post-financial crisis regulations curbed their risk-taking. Bonds bought a year ago have fallen in value because they offer lower interest rates than those sold today, which is fine unless banks are forced to sell them to meet depositors’ demands.

Another concern is the unpredictable behaviour of depositors as they look for more lucrative places to park their cash, including money market funds and crypto, if banks are slow to raise rates for savings.

Below is a rundown of how all this and more is playing out in branches and trading rooms from London to New York.

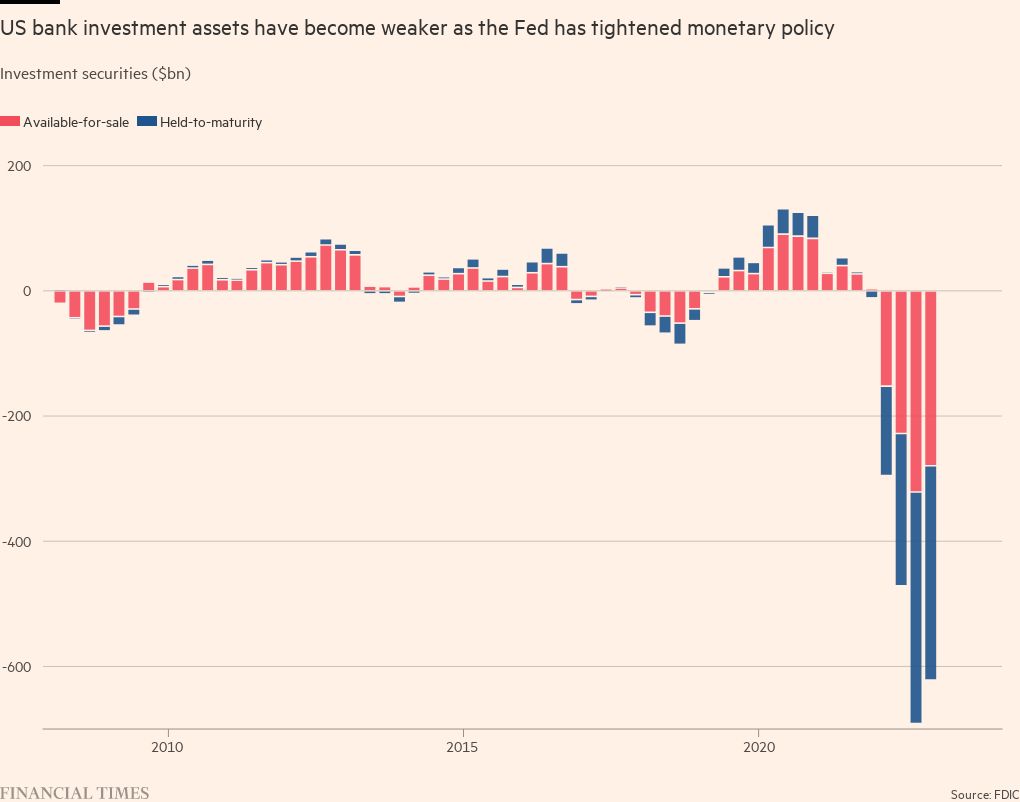

Losses on bond portfolios

Banks routinely buy very safe government debt as a way to meet regulatory requirements to hold a sufficient amount of high-quality liquid assets. Rising rates have sharply driven down the value of such bonds.

The US Federal Reserve said American banks had $620.4bn in unrealised losses on their securities portfolios at the end of 2022, including $340.9bn on bonds they did not plan to sell. Under US rules, lenders do not have to take into account mark-to-market losses in their earnings or capital ratios, so most have not hedged against that possibility.

When a bank finds itself short of cash to meet deposit outflows, as happened to Silicon Valley Bank, it may be forced to sell part of its “held to maturity” portfolio, crystallising losses and potentially spooking both investors and depositors.

The rules are different for banks in Europe, where regulatory capital already reflects the effect of prevailing interest rates on most bonds. In the UK, Numis analyst Jonathan Pierce says the six big UK banks have £600bn of debt securities, of which two-thirds are already carried at fair value.

Writing down the rest of the portfolio to current market prices would hit the banks’ capital ratios by just 30 basis points, he said, a small amount in the context of their average 15 per cent capital ratios which were “more robust than in many banking geographies”.

Analysts say European banks also appear to have hedged much of the rate risk. That eliminates the problem of unrealised losses affecting a bank’s ability to lend, as hits on bond values happen in real time.

Fixed-rate loans

Rising rates pose a dual challenge to the lending side of banks’ asset books.

Those able to pass on rate rises to customers via floating-rate loans enjoyed a surge in earnings in 2022. Fixed-rate loans have less chance of default but they are also a profitability drag for banks whose own funding costs will be increasing.

Higher rates also lead to more defaults, although non-performing loans remain at low levels in the EU where only 1.5 per cent of mortgages were classed as bad loans in September, the latest available European Banking Authority data shows.

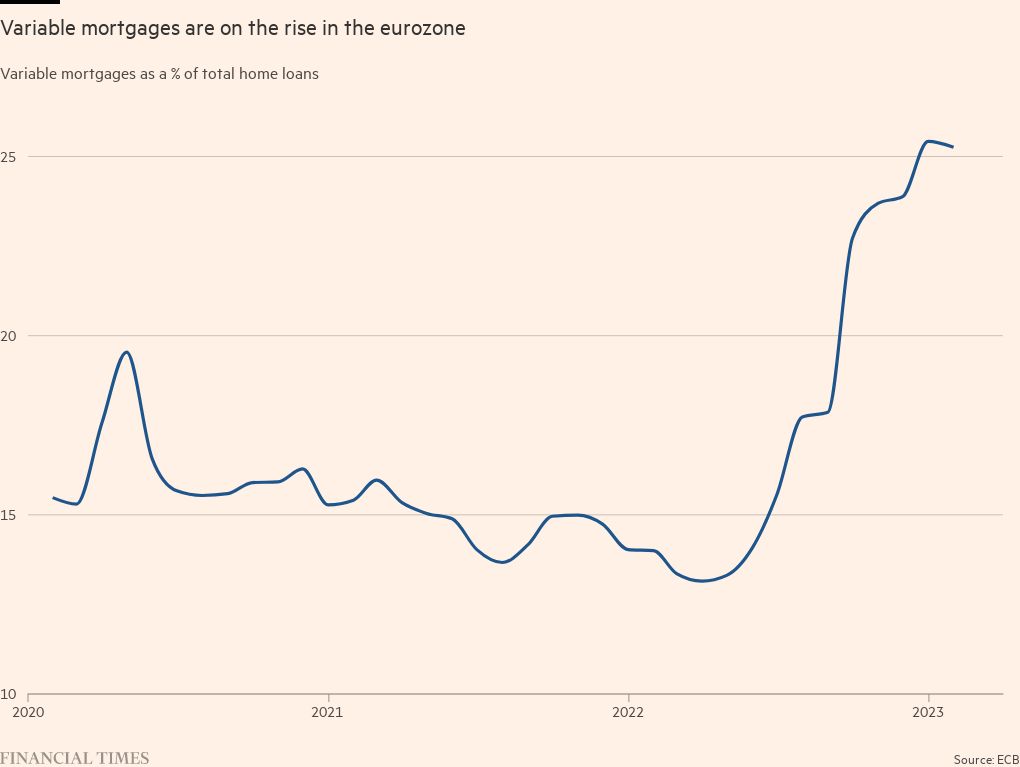

Variable-rate loans are becoming more popular in the eurozone but fixed mortgages still account for about three-quarters of the total, according to European Central Bank data. The proportion varies by country — an ECB study in 2019 found that fixed-rate products made up just 4.5 per cent of mortgages in Portugal but more than 80 per cent in France. In the UK, almost 85 per cent of all mortgage loans were at fixed rates at the end of last year but the percentage for new home loans was almost 95 per cent, data from the Bank of England and Financial Conduct Authority shows.

The picture is more complicated in the US, where adjustable-rate mortgages account for less than 10 per cent of total mortgages but 36 per cent of those held on bank balance sheets, according to Federal Deposit Insurance Corporation data.

Commercial real estate

Commercial real estate loans are particularly in focus for banks. As well as surging interest rates, property investors are facing lower valuations because of pandemic-related changes to work and shopping patterns.

Just over two-fifths of US CRE loans are held by banks, according to JPMorgan.

Fed chair Jay Powell said last week that the central bank “was aware” of concentration in CRE lending but stressed that he did not think the issue was comparable to other strains on banks.

European banks’ exposure to commercial real estate has been identified as a “key vulnerability” by the ECB. However, CRE makes up only about 6 per cent of European loan books, according to asset manager DWS.

Conservative loan-to-value ratios of 50 to 60 per cent in Europe also give banks a healthy cushion to absorb falling prices, according to a Bayes Business School study.

Yet debt costs have doubled in a year and analysts expect turmoil in the banking sector to add to refinancing challenges. “Lending standards going forward will be tighter,” said Zachary Gauge, real estate analyst at UBS. “We haven’t seen an awful lot of forced sales coming through but there are assets that are in trouble.”

Private assets

Another area in focus is banks’ exposure to the burgeoning world of private credit. High on regulators’ watch lists are leveraged loans, which private equity groups typically use to fund their acquisitions.

Leveraged loans typically combine “high leverage, aggressive repayment assumptions, weak covenants, or terms that allow borrowers to increase debt, including draws on incremental facilities”, according to an annual review issued by US regulators last month.

Because such loans attract interest at floating rates, their value does not mechanically fall as rates rise — but that may not help much if overleveraged companies struggle to meet the rising cost of servicing their debts.

Credit to hedge funds that have made big bets on interest rates is another area that banks are carefully monitoring. The Financial Times reported last weekend that US regulators had flagged concerns over one fund, Rokos, which was forced to give extra collateral to banks after its rates bets backfired.

Deposit outflows

When interest rates and inflation rise, savers expect their money to work harder. That does not always happen at banks, which can prompt customers to take their money elsewhere.

In the US, total bank deposits have fallen 3.3 per cent since the Fed began raising interest rates last year, as savers sought out higher-yielding alternatives to the 1 per cent interest many US banks offer, such as the 4 per cent they can get from money market funds.

The trend accelerated around the time SVB and Signature Bank failed. Deposits at US banks declined by the most in almost a year in the seven days to March 15.

Fed data shows that the deposit outflows — which overall amounted to $98.4bn or 0.6 per cent of the total — came from small banks, while there was an increase in deposits at larger rivals.

“We could see a sizeable credit crunch as banks will need to rein in lending due to large deposit flight,” said Kathy Bostjancic, chief economist at Nationwide.

In the eurozone, depositors have withdrawn €214bn over the past five months, or 1.5 per cent of total deposits, according to data published this week by the ECB. The decline accelerated in February, the latest month for which there is data, as depositors cut their holdings by €71.4bn, the biggest monthly fall since records began in 1997.

European banks have been able to replace some deposit funding by issuing covered bonds, which are secured against a pool of home loans, said Luca Bertalot, secretary-general of the European Mortgage Federation.

Funding cost increases

While other funding sources are available, they become more expensive when rates rise as investors demand higher yields.

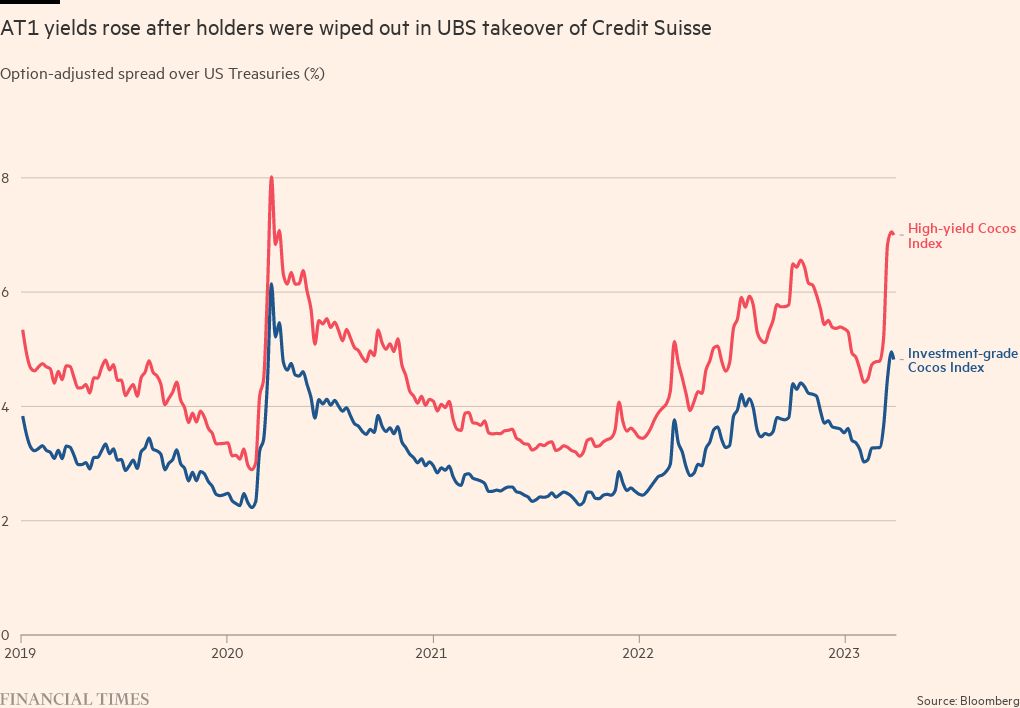

The recent decision by Swiss regulator Finma to wipe out SFr16bn ($17bn) of additional tier 1 bonds as part of the UBS takeover of Credit Suisse will further increase European banks’ wholesale funding costs.

On average, European banks hold AT1 exposure equivalent to 2.2 per cent of their risk-weighted assets, although it is markedly higher at some lenders such as Julius Baer with 7.2 per cent, and Barclays at 3.9 per cent.

“For the second-tier Swiss banks — not UBS but the likes of Julius Baer or Vontobel — there is a fear over whether the market is going to be open for AT1s and, even if it is, at what price?” said an adviser to several banks.

Additional reporting by Mark Vandevelde, Jennifer Hughes and Kate Duguid in New York; Owen Walker and Joshua Oliver in London; Martin Arnold in Frankfurt; and Sarah White in Paris

Comments