The FTX bankruptcy filing in full (updated)

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Here it is: the Chapter 11 declaration from FTX Trading Limited to the District Court of Delaware.

The full statement is well worth your time, as is Kadhim’s backgrounder. Please use the comment box to share your personal highlights.

In terms of a summary the opening remarks from new CEO John J Ray, who’s leading the restructuring of the collapsed exchange, are as good as any:

Never in my career have I seen such a complete failure of corporate controls and such a complete absence of trustworthy financial information as occurred here. From compromised systems integrity and faulty regulatory oversight abroad, to the concentration of control in the hands of a very small group of inexperienced, unsophisticated and potentially compromised individuals, this situation is unprecedented.

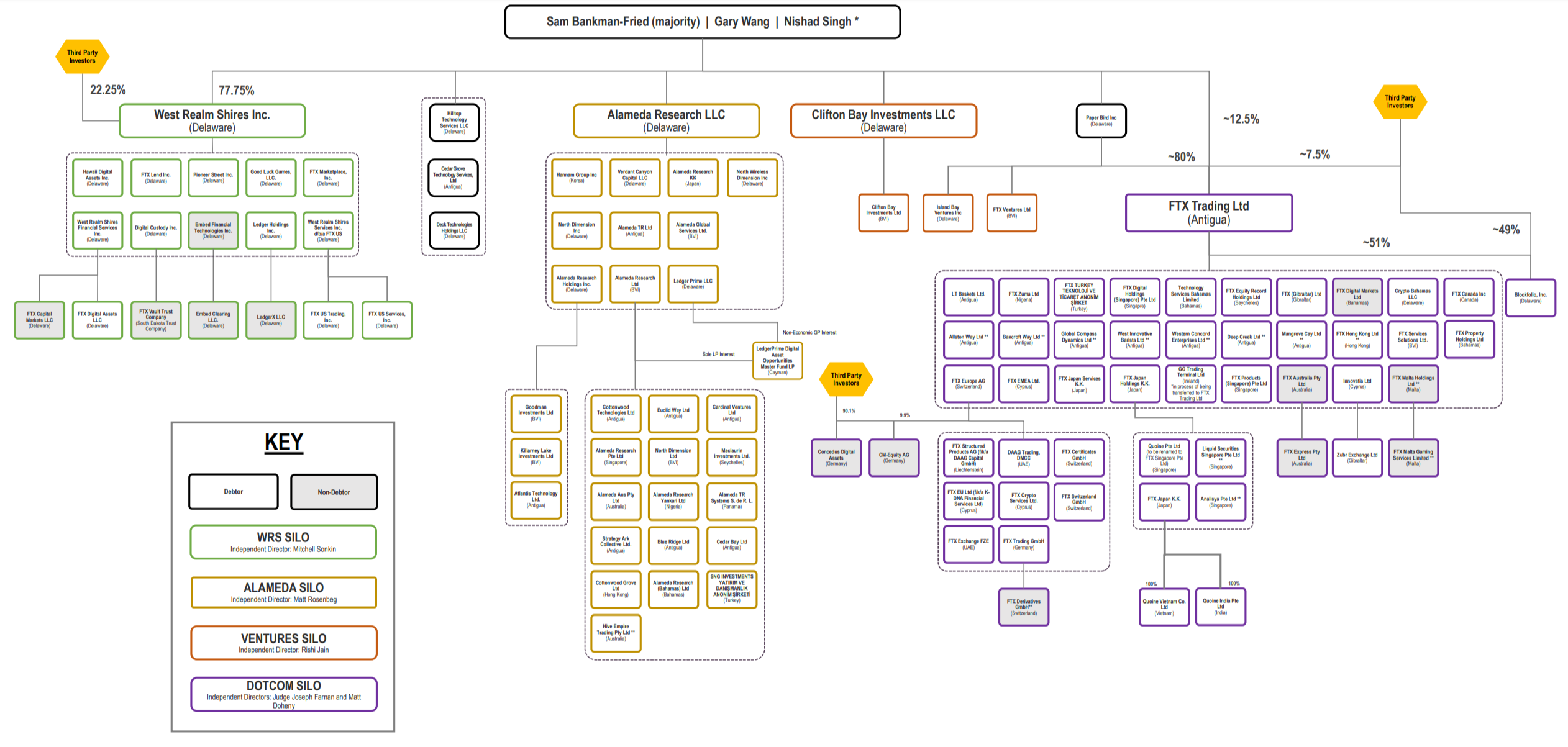

He also has managed to make some sense of the chaos diagram that was FTX’s pre-bankruptcy corporate structure:

And here's the expanded version for the corkboard for those of you following along at home:

[Zoom]

It would be fascinating to dig into the balance sheets in the filing, but the latest documents that Ray had to work with (c. September 30) are missing one extremely important liability: customer crypto deposits.

FTX’s exchanges are “expected to have significant liabilities arising from crypto assets deposited by customers . . . However, such liabilities are not reflected in the financial statements prepared while these companies were under the control of Mr. Bankman-Fried.”

The Alameda and VC divisions also “did not keep complete books and records of their investments and activities”, so their balance sheets will need to be built from scratch.

Rescue attempts will be hindered by “the absence of lasting records of decision-making”, which was “one of the most pervasive failures of the FTX.com business”. SBF “often communicated by using applications that were set to auto-delete after a short period of time, and encouraged employees to do the same.”

There was no daily reconciliation of crypto positions. A software backdoor “conceal[ed] the misuse of customer funds”. User keys and critically sensitive data were sent around the group by an “unsecured group email account”. Group payment requests went “through an online chat platform where a disparate group of supervisors approved disbursements by responding with personalised emojis.” A paper trail is largely non-existent.

“The debtors are writing things down,” Ray says pointedly.

Debtors have enlisted blockchain specialists to follow the money. How to divide up the cash located so far between the various silos is a mystery.

FTX International’s $5.5bn of crypto assets at the end of September had an actual market value of $659,000.

That’s not $659mn, please note. It’s $659k. [Updated to reflect that it wasn’t $659. Though maybe it will be eventually.]

Figuring out what’s owed whom is a shitshow. There’s no top 50 list of creditors yet, because, following the reported hack, checking the repositories “may create a risk of its loss to unauthorised persons”.

If the $300-million-ish hack was carried out by a former FTX employee, as SBF guessed in his DMs with Vox this week, there is some bad news: as of yet, there’s no list of people who actually worked at FTX.

The Debtors have been unable to prepare a complete list of who worked for the FTX Group as of the Petition Date, or the terms of their employment.

Oh, and Ray says that employees and advisers used company money to buy stuff. And it seems like they did that without even filling out the paperwork to make it a loan:

I understand that corporate funds of the FTX Group were used to purchase homes and other personal items for employees and advisors. I understand that there does not appear to be documentation for certain of these transactions as loans, and that certain real estate was recorded in the personal name of these employees and advisors on the records of the Bahamas.

At this point, it’s probably simpler to add bullet points for other jaw-dropping bits:

The amount of cryptocurrency Debtors have been able to secure in cold wallets adds up to $740m. For a reported ~$9bn in total customer deposits.

The “secret exemption of Alameda from certain aspects of FTX.com’s auto-liquidation protocol,” which was presumably necessary to let it lever up to the gills the way it did.

The “dilutive ‘minting’ of approximately $300m in FTT tokens by an unauthorised source” after FTX filed for bankruptcy. That’s along with the $372m hack.

One of the board members appointed by Ray helped restructure Eastman Kodak. Another is advising MBIA Insurance Corp on its exposure to Puerto Rico.

And via one of our excellent commenters, one the firm’s auditors is “Prager Metis, a firm with which I am not familiar and whose website indicates they are the first-ever CPA firm to officially open its Metaverse headquarters in the metaverse platform Decentraland,” says Ray.

“The Debtors do not have an accounting department and outsource this function.”

Lastly, Ray hasn’t been impressed by SBF’s attempts to salvage his reputation with “erratic and misleading public statements”:

Mr. Bankman-Fried, whose connections and financial holdings in the Bahamas remain unclear to me, recently stated to a reporter on Twitter: “F*** regulators they make everything worse” and suggested the next step for him was to “win a jurisdictional battle vs. Delaware”.

F*** or be f***ed; that is the question.

{kind=link}

Comments