H2O Asset Management: illiquid love

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

For the first time in a long time, Lars Windhorst had good news last month.

After several difficult years, which saw the enigmatic and flamboyant German financier facing at least seven lawsuits mostly over complicated financing agreements, Lars Windhorst announced he was back with a full corporate rebrand and a new advisory board that includes fund management heavyweights Martin Gilbert and Avenue Capital’s Marc Lasry.

Hailed as a “wunderkind” in his teens by German chancellor Helmut Kohl, Mr Windhorst might now be better referred to as a “Stehaufmaennchen” for this uncanny ability to bounce back from even the most precarious financial and legal situations.

In the noughties, Mr Windhorst weathered the collapse of two companies, personal bankruptcy, a suspended jail sentence and a plane accident which claimed his ear lobe — all before he was 34.

He then upped sticks to Savile Row in the heart of Mayfair a decade ago, reforming his businesses around a holding company Sapinda — where he developed a reputation for hosting lavish Christmas parties at London’s Natural History Museum.

It wasn’t long before familiar headlines reappeared, however. From 2016 Lars and Sapinda found themselves engaged in legal battles involving at least €220m with several investors — including Ukraine-born billionaire Len Blavatnik.

The lawsuits mostly centred on his failure to settle sale and repurchase agreements of illiquid bonds. One particularly dogged claimant — who FT Alphaville understands to be a Russian former politician — even managed to seize some of Lars’s assets, including a private jet, for a brief period in 2017.

But those particular troubles are now behind him.

Sapinda is now Tennor Holding, with Lars taking the role of chairman of its new advisory board. Lasry and Gilbert are undeniably the biggest names on his revamped board, as co-founder of US hedge fund Avenue Capital and vice-chairman of UK asset manager Standard Life Aberdeen respectively.

But one less widely known name stuck out like a sore thumb to FT Alphaville, if only because he has rather more skin-in-the-game when it comes to Lars Windhorst. Or at least, his clients do. Meet Bruno Crastes.

“There’s no secret”

Proclaimed a “bond maven” by the Wall Street Journal, Bruno Crastes is the chief executive of H2O Asset Management — the firm he established at the start of the decade with backing from Natixis.

The Frenchman has been known to wholeheartedly embrace risk hoping to reap rewards in the longer term, with Mr Crastes perhaps most famous for his big bets on Greek bonds at the height of the eurozone sovereign debt crisis.

H2O has rapidly grown in the past six years: from managing €3bn in 2013, its assets under management have increased ten-fold to €30bn. It’s not hard to see why either, given that some of H2O’s funds were among Europe’s best-performing alternative funds last year. One strategy returned an impressive net 32.9 per cent.

Mr Crastes has been reluctant to go into the specifics of how H2O has been able to beat the market so handily. When our colleagues at FTfm asked him about the magic formula behind his success earlier this year, he was coy:

“There’s no secret,” says Mr Crastes, as we sip H2O’s own-brand water in his chic office in Mayfair, London. The Frenchman is relaxed but reluctant to be seen as a sage. He credits H2O’s performance to “hard work”, experience and a “close-knit” team.

To those who have followed the firm’s investment strategy closely, Bruno Crastes’s relationship with Lars Windhorst is certainly no secret either.

For years, H2O Asset Management has been a notable financial supporter of Mr Windhorst’s fundraising efforts. This included investments in his ill-fated €1bn Sapinda Invest bond which failed to pay its scheduled coupons on time in 2016. The following year Deloitte resigned as auditor of the special-purpose vehicle — accusing its custodian Shard Capital of providing ‘deliberately false’ financial information.

(Shard, for its part, said that any answers it gave the auditor were given in good faith and the broker believed them to be true.)

Now that Mr Crastes’ longstanding association with Mr Windhorst has been made official through the new board seat, we thought it’d be worthwhile to take a closer look at just how much money his funds have invested in the colourful financier’s businesses.

Given that the bonds backing Mr Windhorst's companies are highly illiquid, and H2O’s funds allow retail investors to withdraw their money on a daily basis, the apparent scale of these investments is significant.

“Little, if any, market activity”

First, a note on our methodology.

H2O’s six funds that hold substantial amounts of Windhorst-related bonds — Adagio, Allegro, Moderato, Multibonds, Multistrategies and Vivace — all provide a detailed breakdown of their financial positions every six months.

The dates they report are out of sync, however, so it’s always possible that positions have been moved around the funds internally and our aggregate numbers are out as a result. Despite the limitations, this is the way Bloomberg’s popular “HDS” function calculates aggregate holdings in individual securities, for example.

Using this methodology, H2O appears to hold more than €1.4bn in bonds issued by financial vehicles linked to Mr Windhorst across the six funds. They each hold exposures of between 5.5 per cent (Adagio) to 13.7 per cent (Multibonds) in Windhorst-related bonds.

The data suggest H2O is by far the biggest holder of many of Lars Windhorst’s bonds, often holding the majority of the outstanding amount across the firm and even individual funds holding up to 22 per cent of specific securities.

A bond issue from Chain Finance, a vehicle that Mr Windhorst used in 2017 to settle outstanding lawsuits and repay existing debts, proved a particularly popular investment for H2O. All six funds poured money into it, together they hold a combined €383m of the €500m bond — nearly 77 per cent.

In the case of Chain Finance, H2O has explicitly acknowledged that its investment is not exactly liquid. The fund manager applies what it calls a “a haircut related to the illiquidity of the value” on its holding in the bonds, marking it down significantly in its portfolio (the market value is 24 per cent less than face value across the funds).

Interestingly though, this approach is not adopted on any of its other Windhorst-related securities, which are equally illiquid according to several people familiar with the bonds.

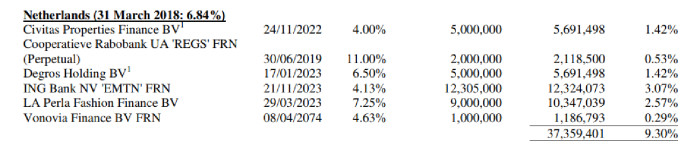

It is instructive to contrast how other bondholders mark them. In the case of Civitas Properties' and Degros' bonds — of which H2O holds 58 per cent and 36 per cent — we looked at the only other publicly reporting fund that owns both: Rubrics Asset Management.

Rubrics is the fund management arm of Shard Capital — the same firm Deloitte accused of providing ‘deliberately false’ financial information on behalf of Mr Windhorst’s Sapinda Invest. Interestingly, its holdings in Civitas and Degros carried footnotes in its annual report last year:

The footnote explains that both investments are marked as Level 3 assets, meaning that it used “unobservable inputs” (ie not market prices) to value the securities. It goes on to say that it does this when “there is little, if any, market activity for the asset or liability at the measurement date”.

H2O in contrast appears to use market inputs to value them. We asked Mr Crastes about the amount of Lars Windhorst related debt he held and the liquidity of these investments. He declined to comment, explaining that the “official policy of H2O AM is to never comment on the underlying positions of our funds”.

“Significant discrepancies with the valuation price”

H2O appears to have previously sailed close to the wind with its use of market inputs to value Lars Windhorst’s bonds.

In 2016, the auditor of its funds PwC included a qualification related to H2O’s holding of the aforementioned Sapinda Invest bond. The audit firm explained that while the asset manager had used a price contributed by an intermediary, market prices for the notes from other sources had “significant discrepancies with the valuation price”.

In plain English, the price from a broker that H2O used to value bonds was much higher from those of other dealers. How much higher? Well PwC said that the discrepancy may have represented more than 1 per cent of the net assets of one of H2O’s funds:

But don’t worry readers, the troubling episode had a happy ending for H2O. Their position in Sapinda Invest’s bonds got taken out the following year at the same price it was marked at, as detailed in their annual report:

What happened in September 2017? Well, Lars Windhorst issued another bond!

In September 2017, Lars raised the previously mentioned €500m Chain Finance bond. As we reported at the time, the investors in this bond were primarily rolling over their existing exposures to Windhorst securities:

“The thinking is that, if you give him three years, maybe his operating companies will be profitable, while if you force him to repay everything now you could be fighting over scraps,” said one of the people familiar with the deal. “The people who own existing bonds want to play ball. If you have an exposure, you amend and extend.”

In other words: H2O replaced its Sapinda Invest bonds with new Chain Finance bonds. And, crucially, those Sapinda notes were repaid at a price consistent with the valuation that PwC had earlier raised concerns around.

Follow the flows

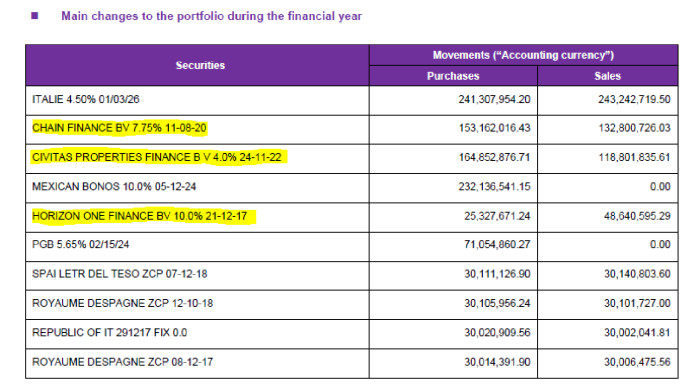

H2O’s flows in and out of Lars Windhorst’s myriad special-purpose vehicles have in the past formed a significant part of their trading activity.

In this extract from their Multibonds fund’s 2017 annual report, you can see that three Windhorst-related bonds were in their top five portfolio movements that year. It is stark to see three obscure SPVs linked to a German financier with a questionable business record nestled among a list of government bonds:

And there are signs that newly minted bonds linked to the former “wunderkind” are now flowing into H2O’s portfolios.

Mr Windhorst appears to have been busily issuing new bonds in the past few months. There is, for instance, Netherlands-registered Trent Petroleum Finance, which issued a €850m bond in December last year.

For those familiar with Mr Windhorst’s ventures, Trent Petroleum Finance BV is the new name for what was previously Centrics Oil & Gas Finance BV.

And just on Monday, he closed a new €1.5bn bond issue from the entity Tennor Finance BV.

Other new bond issues appear to be Everest Medtech and Rubin Robotics. These two entities are held by a Dutch entity called “Stichting Horizon One”, which is also the parent company of the aforementioned Chain Finance, according to the Orbis database, published by Bureau van Dijk.

A “stichting” is an orphan entity under Dutch law, that is one that technically doesn’t have an owner. One notable feature is the structure's ability to isolate assets from any legal claims at related entities, which is why it is commonly used in Dutch securitisations, but could also prove useful if you were the subject of repeated litigation.

In the past six months, Trent Petroleum, Rubin Robotics, Tennor Finance and Everest Medtech have issued a total of €2.75bn in bonds at yields between 5 and 8 per cent. And they are starting to appear in H2O’s filings.

The French fund manager holds €247m of Trent’s €850m bond across four of its funds, as of March 2019. That’s nearly 30 per cent of the debt issue, whose proceeds are earmarked for refinancing, energy investments and general corporate expenses. Everest Medtech has appeared in the “Netherlands” section of H2O Adagio’s March 2019 filings.

“H2O Asset Management is one of many institutional investors supporting our investment strategy and co-investing with us across different assets,” a spokesman for Mr Windhorst's Tennor Holding told FT Alphaville, when we asked them about the French fund manager's large holdings of related securities.

“Hiding in plain sight”

You might well ask: why does this matter?

After all, H2O’s funds are making great returns. While many would blanch at the prospect of investing well over €1bn with an entrepreneur widely known for his legal difficulties, perhaps Mr Crastes has once again spotted an opportunity to make money where others fear to tread.

And as we’ve explained, these positions are not secret — they’re all publicly disclosed in H2O’s reports.

Despite all this, the large exposure Mr Crastes’ firm has built up to Lars Windhorst’s businesses matters because of the liquidity of these investments.

Lars Windhorst’s bonds are not widely traded. In the case of Chain Finance, H2O itself acknowledges the illiquidity risk, but this applies to debt across his web of interrelated companies.

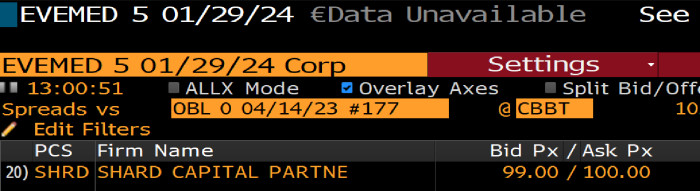

For example, the only broker listed as quoting the new Everest Medtech bond on our Bloomberg terminal is Shard Capital — the same firm that Deloitte rebuked for its alleged conduct over the ill-fated Sapinda Invest bond:

There’s a reason these bonds are not widely traded. Several traders and hedge fund managers told us that certain banks have restrictions on trading securities related to Lars Windhorst, due to the number of financial institutions that were ensnared in failed trades on bonds and shares of his companies.

There was the time Citi found itself briefly exposed to a $400m hit on a repo primarily on Lars Windhorst-related bonds, or the instance of Goldman’s failed repo with an Abu Dhabi brokerage that had links to Lars.

(Goldman fired a director over the incident who then filed a suit against the bank, alleging that it had tried to “pin the blame” on him for a series of trades with an unnamed “notorious European businessman”. Mr Windhorst has previously denied he is the subject of the dispute. H2O has also invested in the debt of the Middle Eastern brokerage — ADS Securities — although we have left that out of our calculations.)

While these bonds are undeniably illiquid, H2O’s funds are all in Ucits format, allowing retail investors to freely take their money out on a daily basis. These EU rules are supposed to cap the amount of illiquid investments, but we are increasingly seeing the dangerous consequences of fund managers obeying the letter but perhaps not the spirit of the law.

Just look at Neil Woodford, the star UK fund manager whose eponymous investment firm is now falling apart after he had to prevent investors from withdrawing money from a flagship fund a fortnight ago.

Mr Woodford struggled to meet demands for money back because of his Ucits fund's high percentage of investments in illiquid assets. Yet he’d used ingenious methods to technically comply with the regulation, such as getting unquoted companies to list on a light-touch Channel Islands exchange.

The incident has exposed how managers are able to find perfectly legal loopholes in the Ucits rules, that on paper only allow up to 10 per cent of assets to be held in less liquid securities — a bucket often known in the industry as the “trash ratio”.

While Mr Woodford’s stricken fund invested in equity not debt, the bond market had its own fund blow-up illustrating the dangers of a liquidity mismatch last year.

Switzerland’s GAM suspended the star manager of its SFr11bn Absolute Return Bond Funds in July last year, with little public explanation. Investors panicked, and began pulling money out of the manager's funds, before GAM gated the funds to prevent investor withdrawals. It then took the drastic decision to start liquidating the funds entirely, an outcome that stunned observers given this was a supposedly diversified fund in a comparatively benign market.

The full story involves trips on private jets with an Indian-born industrialist and an Australian financier closely linked to David Cameron, so we strongly recommend that you read the FT’s deep dive into the debacle if you haven’t already done so. But the short explanation of why GAM’s star investment strategy unravelled so suddenly: portfolio manager Tim Haywood had invested large amounts of the capital into highly illiquid bonds, while also letting investors in and out on a daily basis.

The really interesting thing, however, is GAM's insistence that Mr Haywood did not breach the funds’ rules by holding these investments.

Mr Haywood invested large sums in highly illiquid bonds structured by the firm Greensill Capital, which was set up by the divisive Australian financier Lex Greensill. Many of these were linked to the sprawling business empire of Indian steel magnate Sanjeev Gupta. Mr Haywood’s funds frequently owned the majority, if not all, of these debt issues.

The exposures were split up between several SPVs, however. Each on its own did not look particularly worrisome. But an FT analysis of GAM’s main Luxembourg-domiciled fund’s reported holdings showed that, a month before Haywood’s suspension, nearly 12 per cent of the fund was invested in Greensill-related paper for several different borrowers.

To anyone willing to trawl through GAM’s filings and dig into what these obscure SPVs were, the danger the bonds posed was clearly laid out. But it wasn’t until investors tried to withdraw their money that they discovered the problem. Or as one GAM investor told the FT in March:

The Gupta bonds themselves, however, were no secret; they had been listed in the funds’ semi-annual report for the end of 2017. “They’ve been hiding in plain sight,” says one investor.

Comments