How China’s tech bosses cashed out at the right time

Simply sign up to the Technology sector myFT Digest -- delivered directly to your inbox.

In China, there is no clearer sell-sign than when Xi Jinping, the Chinese president, starts personally attacking an industry.

So when Xi complained in March that relentless home-schooling was a “stubborn disease” that was putting too much pressure on Chinese children and their parents, the heads of at least two Chinese tutoring companies started selling their shares in New York.

In one previously unreported trade, a shell company holding shares for executives at GSX Techedu, whose market capitalisation in New York was about $24bn at the time, launched the sale of shares worth as much as $119m just three days after Xi spoke.

The sale is among hundreds of records reviewed by the Financial Times that provide one of the first looks at how and when executives at China’s biggest New York-listed tech companies trade their shares.

In public, Larry Chen, the chief executive of GSX, who does not appear to be linked to the shell company that sold, expressed confidence in his business, promising at the end of March to buy $50m of shares with his own money.

But one person close to GSX said its leaders were aware at the time of the trade that Beijing was considering stricter regulations on the industry.

By July, the Chinese government had banned the entire sector from making profits, crashing the share prices of all the major tutoring companies. Today, the block of GSX shares that was put up for sale in March would be worth only $4m. Chen does not appear to have yet fulfilled his $50m pledge.

GSX (which has since rebranded as Gaotu Techedu) declined to comment on the share sale and said any share purchases by Chen would be noted in public filings. None has so far occurred.

In the run-up to the July profits ban, executives at another Chinese education company also cashed in their NY-listed shares.

The husband and wife team who co-founded online English tutoring platform 51Talk began selling shares on April 1 and sold blocks of shares roughly every other day through to the end of June. Their sales represented as much as half the traded shares on a few days. By the time Beijing announced its new regulations, they had cashed out $4.3m. 51Talk did not respond to repeated requests for comment.

The documents reviewed by the FT show dozens of other well-timed sales by Chinese executives. While there is no proof of insider trading, many of the deals came ahead of regulatory action or the release of disappointing earnings reports.

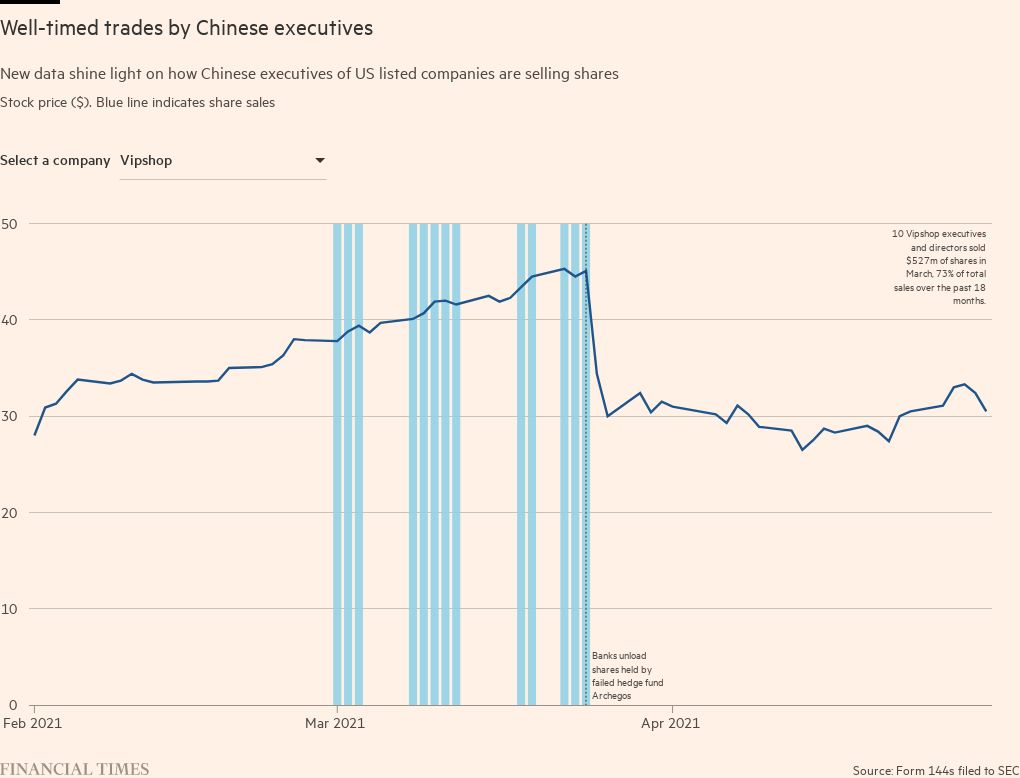

Some executives appear to have hit the top of the market. Ten executives and directors at VIPshop, an online discount shopping site, sold about $527m of shares in March, almost three-quarters of all the shares they sold over the past 18 months, just before the collapse of Archegos Capital Management triggered a sell-off in its shares. Its share price is currently down 70 per cent from its level in March. VIPshop declined to comment.

The trades by Chinese executives have been little noticed because they are held to different reporting rules by the US Securities and Exchange Commission, which insists that US executives have to report share sales within two days. In Hong Kong, directors have three days to report, while executives of companies listed in mainland China must give 15 days’ notice before they can sell.

By contrast, executives at foreign companies listed in the US instead tend to report their total shareholding once or twice a year, or not at all, depending on the size of their stakes. Companies including the online shopping giant Alibaba have used their US listings to gain exemptions in Hong Kong, arguing that any additional disclosure is “unduly burdensome” on its “corporate insiders”.

In the US, under Rule 144, foreign executives have to report when they initiate plans to sell restricted stock either by uploading documents to EDGAR, the main disclosure system, or by mail.

Nearly all of them have historically filed by mail, and the SEC permitted access to the documents in its Washington DC reading room but did not upload them to EDGAR. Since last April, the SEC has also accepted email notifications, but does not upload these to EDGAR either. A private company digitised the filings to sell to institutional investors and banks.

“This system exists not because there are some people that say, yeah, we don’t think foreigners need to report their insider trades — it exists because people haven’t recognised the asymmetry in disclosure rules,” said Daniel Taylor, a corporate finance expert at the Wharton School.

“When I tell people that the trades are reported, but mailed-filed with the SEC, few people believe me until I show them the actual mail filings,” he added.

The SEC is considering changing its rules to mandate all Form 144s be filed to EDGAR.

Some Chinese tech executives also use shell companies which conceal their identities. One top Alibaba executive has used a Bahamas shell company called Sky Scraper Enterprises Ltd to initiate plans to sell shares worth hundreds of millions of dollars.

One plan was launched to sell as much as $155m of shares in the weeks around the planned blockbuster IPO of Alibaba’s sister company Ant Group. The plan stumbled after Beijing intervened to block the IPO.

While the identity of the executive could not be proven, there were some clues: he or she won larger and larger share packages over the past decade and is among the company’s best-compensated leaders. The FT identified different shell companies used by almost all of Alibaba’s top brass, except for chief executive Daniel Zhang and Eric Jing, the chair of Ant.

Alibaba said it had “a strict policy and rigorous procedures in place to ensure that all our employees, especially our directors and officers, fully comply with all applicable securities laws”. The spokesperson added that all executive officers must sell shares according to passive plans with 30 or 60-day cooling off periods before trades automatically execute. Ant declined to comment.

Planned trading schemes are ostensibly intended to prevent any unlawful insider trading, but Taylor has done research that shows their potential for misuse. Several Chinese executives made well-timed trades under plans adopted at the end of the companies’ financial quarters, raising concerns that they could have made them while being aware of forthcoming quarterly earnings.

In 2016 and 2017, the chief executives of New York-listed Cheetah Mobile and Tarena International initiated the sale of shares worth as much as $31m and $10m a few weeks before reporting quarterly results that sent their share prices down 30 per cent and 24 per cent, respectively. Both men had adopted the trading plans at the end of the quarter.

“This is a big red flag. The fact that these plans were adopted at quarter-end and initiated trades prior to the earnings announcement is highly concerning,” said Taylor.

Cheetah Mobile did not respond to repeated requests for comment. Tarena declined to comment.

Additional reporting by Hudson Lockett in Hong Kong

Comments